10-K: Annual report pursuant to Section 13 and 15(d)

Published on February 24, 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended | |||||

Commission file number: 1-7945

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

||||||||||

(Address of principal executive offices) |

(Zip Code) |

||||||||||

Registrant’s telephone number, including area code: (651 ) 483-7111

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☑ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☑ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Accelerated Filer | ☐ | ||||||||||

| Non-accelerated Filer | ☐ | Smaller Reporting Company | |||||||||

| Emerging Growth Company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☑ No

The aggregate market value of the voting stock held by non-affiliates of the registrant is $924,918,940 based on the last sales price of the registrant's common stock on the New York Stock Exchange on June 30, 2022. The number of outstanding shares of the registrant's common stock as of February 8, 2023 was 43,266,924 .

Documents Incorporated by Reference: Portions of our definitive proxy statement to be filed within 120 days after our fiscal year-end are incorporated by reference in Part III.

DELUXE CORPORATION

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2022

TABLE OF CONTENTS

| Item | Page | |||||||||||||

2

PART I

Please note that this Annual Report on Form 10-K contains statements that may constitute “forward-looking statements” under the Private Securities Litigation Reform Act of 1995 (the "Reform Act"). Forward-looking statements include information concerning future strategic objectives, business prospects, anticipated savings, financial results (including earnings, liquidity, cash flow and capital expenditures), industry or market conditions, demand for our products and services, acquisitions and divestitures, anticipated results of litigation, regulatory developments or general economic conditions. Because actual results may differ materially from those expressed or implied by these forward-looking statements, we caution readers not to place undue reliance on these statements. Our business, financial condition, cash flows and operating results are influenced by many factors, which are often beyond our control, that can cause actual results to differ from those expressed or implied by the forward-looking statements. Part I, Item 1A of this report outlines known material risks and important information to consider when evaluating our forward-looking statements. The Reform Act provides a “safe harbor” for forward-looking statements to encourage companies to provide prospective information. When we use the words or phrases “should result,” “believe,” “intend,” “plan,” “are expected to,” “targeted,” “will continue,” “will approximate,” “is anticipated,” “estimate,” “project,” “outlook,” "forecast" or similar expressions in this Annual Report on Form 10-K, in future filings with the Securities and Exchange Commission, in our press releases, investor presentations and in oral statements made by our representatives, they indicate forward-looking statements within the meaning of the Reform Act. Readers are cautioned that all forward-looking statements are based upon current expectations and estimates and apply only as of the date of this report. We assume no obligation to update this information.

| ITEM 1. BUSINESS | ||

| OUR BUSINESS | ||

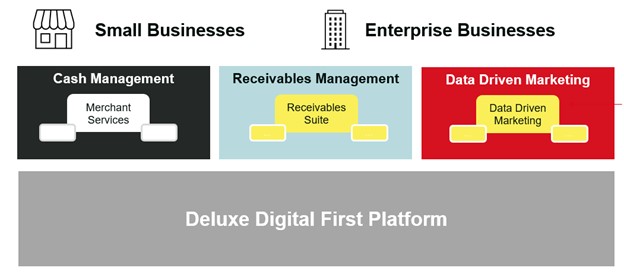

More than 105 years ago, Deluxe Corporation began providing payment solutions. Our longevity is a testament to our innovation, our ability to evolve with our customers, and the trust they place in us. We are no longer solely a check printing company, but have transformed to a Trusted Payments and Data CompanyTM that champions business so communities thrive. We support millions of small businesses, thousands of financial institutions and hundreds of the world's largest consumer brands, while processing approximately $3 trillion in annual payment volume. We operate primarily in the U.S., but we also sell our products and services in Canada and portions of Europe and South America. We operate 4 business segments that are generally organized by product type. These segments provide the following products and services:

| Business Segment | Category | Percentage of 2022 consolidated revenue | Description | |||||||||||||||||

| Payments | Merchant services and other payment solutions | 19.5 | % | Merchant in-store, online and mobile payment solutions; payables as a service, including eChecks, Medical Payment Exchange and Deluxe Payment Exchange; payroll and human resources services; fraud and security services | ||||||||||||||||

| Treasury management solutions | 10.8 | % | Receivables as a service, including remittance and lockbox processing, remote deposit capture, receivables management, and payment acceptance | |||||||||||||||||

| Total | 30.3 | % | ||||||||||||||||||

| Data Solutions | Data-driven marketing solutions | 7.9 | % | Solutions for marketing business-to-business and business-to-consumer | ||||||||||||||||

Web and hosted solutions |

4.0 | % | Web hosting and software-as-a-service (SaaS) solutions, including web design, logo design, financial institution profitability reporting, and business incorporation services | |||||||||||||||||

| Total | 11.9 | % | ||||||||||||||||||

| Promotional Solutions | Forms and other products | 13.0 | % | Business forms and accessories, including envelopes, labels, stationery and more | ||||||||||||||||

| Marketing and promotional solutions | 12.2 | % | Advertising specialties, promotional apparel and print services | |||||||||||||||||

| Total | 25.2 | % | ||||||||||||||||||

| Checks | Checks | 32.6 | % | Printed business and personal checks | ||||||||||||||||

3

We sold our Australian web hosting business during 2022 and expect to complete the sale of our North American web hosting and logo design businesses in the first quarter of 2023, after which we will have completed an intentional strategic exit from this market.

| OUR STRATEGY | ||

Our vision is to be a trusted technology partner empowering businesses to pay, get paid and grow. To realize this vision, we will continue to leverage our strengths.

•Our customers – Our products and services are utilized by customers of all sizes and maturities. We continue to benefit from a long heritage of offering trusted service to our customers, which in turn, fuels meaningful cash flow that is redeployed to invest in our products, infrastructure and growth opportunities.

•World-class payments and data products and platforms – We continue to invest in market-leading payments and data products and platforms that are proprietary to Deluxe, encouraging our customers to build their businesses on our platforms for the long-term.

•Scale – We believe our volumes for many of our service offerings enable us to offer per-unit costs and reliability superior to our competitors. We will continue to focus on scaling our technology and product management capabilities.

•Sales and distribution channels – We have extensive market reach, with millions of small business and consumer customers and thousands of financial institution clients. We will continue to maximize the deployment of these resources, including our sales force and our various strategic relationships, to cost-effectively reach customers.

Since 2019, our focus has been on our transformational strategy, moving from a traditional manufacturing “company of companies” to a more technologically focused “company of products.” We worked to integrate the numerous technology platforms we obtained over the years through our various acquisitions to achieve a connected, modern technology platform. We assembled a talented management team and built an organization focused on developing new and improved products. As a result, we are realizing the benefit of significant new client wins in all of our segments, and in 2022, we generated consolidated sales-driven revenue growth for the second consecutive year. In June 2021, we completed the acquisition of First American Payment Systems, L.P. (First American), a large-scale payments technology company that provides partners and merchants with comprehensive in-store, online and mobile payment solutions. The acquisition enables us to expand significantly in the fast-growing payments sector, a sector known for generating significant recurring revenues and cash flows, and revenue from our growing Payments segment is expected to surpass that of our Checks segment during the first half of 2023. We now have an even stronger foundation from which to pursue future acquisitions or strategic partnerships that will allow us to potentially realize significant revenue synergies, and we believe that our scaled back-end processing will readily support incremental volume.

Moving into the next stage of our transformation, we remain focused on strategic growth and scaling our operations. This includes maximizing our payments and data products, increasing recurring revenue streams, strengthening our talent and culture, and accelerating our portfolio rationalization efforts. For example, we sold our Australian web hosting business during 2022 and expect to complete the sale of our North American web hosting business in the first quarter of 2023. We also sold two smaller product lines within our Promotional Solutions segment. The sale of these businesses allows us to focus our resources on the key growth areas of payments and data. As we invest in these growth areas, we continue efforts to lower costs and simplify and eliminate duplicative processes. We continue to review our real estate footprint, and in 2022, we closed 6 facilities, in addition to the 40 facilities we closed during 2021 and 2020. We are continually refining our operating model to match expected customer needs and anticipated volumes, as well as to gain efficiencies.

| UPDATE ON COVID-19 IMPACT ON OUR BUSINESS | ||

The health and safety of our employees, our customers and their families is always our top priority. As of the date of this filing, all of our facilities are fully operational. When COVID-19 struck, we implemented a variety of new policies and procedures, including additional cleaning, social distancing, and significantly restricting on-site visitors, to minimize the risk to our employees of contracting COVID-19. While many of these precautions have been relaxed or eliminated as the health risk of COVID-19 has decreased, we may need to reinstitute and/or modify these policies and procedures as necessary should the health risk return to an unacceptable level. In such an event, our businesses or our suppliers could be impacted further by supply chain disruptions, which together with other factors such as a shortage of labor, could result in longer delivery times and restricted manufacturing capacity for certain of our products. Governmental actions in response to a resurgence of COVID-19 could also temporarily limit our business activities and those of our suppliers.

Emerging from the COVID-19 pandemic, we have experienced labor shortages, material and delivery inflation, and supply chain disruptions, including impacts on the supply of certain higher margin printed products in our Promotional Solutions segment. We experienced inflationary headwinds across all of our segments during the year ended December 31, 2022;

4

however, these impacts were largely mitigated, with some time lag, through price increases, when possible. We expect inflationary pressures to continue into fiscal 2023, and this trend could have a materially adverse impact if inflation rates significantly exceed our ability to continue to achieve price increases or if such price increases adversely impact demand for our products.

We will continue to actively monitor the situation and may take actions that impact our operations as may be required by federal, state or local authorities or that we determine are in the best interests of our employees, customers, suppliers and shareholders. The extent of additional adverse impacts on our financial condition and results of operations will be dictated by the currently unknowable duration and severity of COVID-19 and its variants, and individuals', companies' and governments' responses to the pandemic, inflation and other macroeconomic conditions.

| SALES AND MARKETING | ||

Everyone sells at Deluxe. We employ a customer-focused approach, deploying dedicated sales teams across our 4 business segments to ensure we leverage the expertise within each segment to meet our customer's needs. Our customers rely on our solutions and platforms to help their finance and marketing teams pay, get paid and grow their business (as illustrated below), allowing our business segments to help each other deliver greater value for our customers and enabling our customers to build their businesses on our platforms for the long-term.

We employ a multi-channel sales and marketing approach, selling directly to financial institutions and major global brands. We also sell our products and services through scalable partnerships, enabling us to cost-effectively reach customers, specifically leveraging our financial institution partnerships, our e-commerce assets and other strategic partnerships. In addition, millions of in-bound customer contacts buying or re-ordering our products and services provide extensive cross-sell opportunities.

| INDUSTRY TRENDS AND OUR COMPETITION | ||

Payment solutions, including checks

The payments industry continues to expand and evolve, with digital payment vehicles and transaction volumes growing around the world. The industry is continuously changing, highly innovative, and increasingly subject to regulatory scrutiny and oversight. The challenge for payment providers is to continually modernize their infrastructure to support new service offerings and to identify new revenue streams, as well as to invest in cloud computing and other digital technologies to more rapidly address evolving customer preferences. This pace of change puts pressure on payment providers to transform and adapt in order to remain competitive.

Competition in the payments industry is intense. We are competing against numerous financial technology (Fintech) companies, including independent payment processors, credit card processing firms and treasury management service providers, as well as financial institution in-house capabilities. Volume is the key to staying cost-competitive, as it allows us to drive scale in our operations, and breadth of services is critical to staying relevant to customers. We believe our competitive advantages are: our scalable platform, extensive distribution channels, superior end-customer experience, frictionless payments (i.e., non-disruptive for payer, and payment choices for payee), automated receivables management, a strong balance sheet and

5

a trusted and respected brand. We also believe there is growth potential for our Medical Payments Exchange (MPX) and Deluxe Payments Exchange (DPX) platforms, which convert paper checks to digital payments.

Our Checks business remains an important part of our strategy. We believe there will continue to be demand for personal and business checks for the foreseeable future. However, the total number of checks written in the U.S. has been in decline since the mid-1990s. The cash flow generated by our Checks business partially self-funds our growth investments. Our check programs are also an important source of lead generation for cost-effective cross-selling of other products and services.

Our Checks business faces significant competition from another large check printer in our traditional financial institution sales channel, direct mail and internet-based sellers of personal and business checks, check printing software vendors, and certain significant retailers. Pricing continues to be competitive in our financial institution sales channel, as financial institutions seek to maintain their previous levels of profitability, even as check usage declines. We believe our competitive advantages come from our design and customization options, our quality and service, the trust our customers have in us, and our strong financial position. In addition, our digital and print-on-demand technology allows us to implement new customer requirements faster and expand our premium check and overall print design options.

Data Solutions

Data-driven marketing – With increased competition among businesses to target and engage new and existing customers, the use of data-driven marketing has continued to increase and evolve. Competition in this industry is intense, with a wide variety of companies in the data solutions space, including advertising agencies, marketing technology firms, data aggregators and brokers, and source data providers. Adapting to new technology is a key challenge in this industry, along with hiring and retaining the right people. We must continually adapt to the changing needs of our customers and expand our offerings to provide a greater breadth of services.

We believe we have significant growth opportunity in this market. We continue to simplify and integrate our separate businesses operating in this market, monetize the significant amount of data we process across the company, invest in technologies, such as artificial intelligence and machine learning, and consolidate our data infrastructure to reduce costs. We also believe that our pay-for-performance offerings provide us a competitive advantage, as our customers value that they get the highest return on their marketing and advertising dollars.

Web and hosted solutions – The market for web hosting services is highly competitive and commoditized, requiring significant spending on product development and customer acquisition to effectively compete in this space. Our business was largely a white label service offered through telecom partners which did not allow for material cross-selling opportunities and did not fit within our overall portfolio. Accordingly, we have strategically moved to exit this business. We sold our Australian web hosting business during 2022 and expect to complete the sale of our North American web hosting and logo design businesses in the first quarter of 2023.

Promotional Solutions

The market for business forms and certain business accessories has been declining for several years, as continual technological improvements have provided businesses with alternative means to execute and record business transactions. Greater acceptance of electronic signatures has also contributed to the overall decline in printed products. The markets for business forms and promotional products are highly competitive and fragmented. Current and potential competitors include traditional storefront printing companies, office superstores, wholesale printers, online printing companies, small business product resellers and providers of custom apparel and gifts.

We believe that our competitive advantages include our multi-channel experience, ease of use, deep sources of supply and breadth of selection of branded apparel and promotional merchandise. We also believe that, by expanding our product set and driving integration of physical and digital solutions, we will transition this segment to a technology-driven business that can respond quickly to market opportunities and differentiate us from our competitors.

| OUR OPERATIONS / SUSTAINABLE PRACTICES | ||

We continue our focus on improving the customer experience by providing excellent service and quality, while increasing our productivity and reducing our costs. We accomplish this by embedding lean operating principles into our processes, while emphasizing a culture of continuous improvement. We utilize a shared services approach, which allows our businesses to leverage shared facilities to optimize capacity utilization and to enhance operational excellence. We continue to reduce costs by utilizing our assets and technologies more efficiently and by enabling employees to better leverage their capabilities and talents.

We have formed an Enterprise Environmental, Social and Governance ("ESG”) Council that is led by our Chief Compliance Officer, with participation from our executive leadership team and senior-level staff, including our General Counsel

6

and Vice Presidents representing our real estate, operations, and human resources functions. This council assesses and monitors our top enterprise ESG risks, goals and strategies and provides updates to our board of directors.

We have implemented a stakeholder-focused ESG program in order to meet the needs and expectations of regulators, our customers, shareholders and employees. We devote significant resources to addressing ESG throughout the enterprise, including waste reduction and process improvement efforts, enhancing our commitments to diversity, equity and inclusion (“DEI”) through our DEI Council and employee resource groups, promoting community awareness, giving back through our volunteer time off program, and continually improving our cybersecurity and privacy processes and controls to keep our data safe. We measure our ESG goals and impacts through yearly strategic assessments that keep us accountable and inform our annual and multi-year ESG strategies.

Sustainability is also embedded into our operational model. We take sustainability seriously and focus on the following areas:

•Energy – We implemented several energy-saving measures during last year's construction of our facilities in Atlanta and Minneapolis, including installing LED lighting, daylight harvesting strategies, optimized HVAC systems and material selections that reduce carbon input and increase recycled content.

•Waste – We are focused on understanding the waste stream in all of our facilities, with the goal of reducing the amount of waste we generate and recycling as much of our waste stream as practicable. We have moved from volume inventories of custom inks to onsite mixing systems. This has greatly reduced waste stream processing, with an added benefit of better response times for customers.

•Materials – Over 90% of our check and forms paper is purchased from Forest Stewardship Council-certified supplier mills. In addition, our vinyl checkbook covers are produced using a minimum of 45% post-industrial recycled material. We also employ recycling efforts that allow us to divert more of our waste out of landfills by being diligent in the segregation of our waste streams.

•Carbon – We continue to review every aspect of our business, including the materials we use, how we manage our facilities and the the role we play in communities, to ensure our growth includes sustainable practices.

Protecting the environment and our shared future is key to our business and to delivering the products our customers need.

| CYBERSECURITY | ||

We are a trusted partner to enterprises of all sizes, and this is a responsibility we take seriously. The secure and uninterrupted operation of our networks and systems, as well as the processing, maintenance and confidentiality of the sensitive information that resides on our systems, is critical to our business operations and strategy. Each year, we process hundreds of millions of records containing data related to individuals and businesses. In addition, many of our products are hosted solutions, and the amount of data we store for our customers on our servers, including personal, important business and other potentially sensitive information, has been increasing. Technology-based organizations such as ours are vulnerable to targeted attacks aimed at exploiting network and system applications or weaknesses. A successful cyberattack could result in the disclosure or misuse of sensitive business and personal information and data, cause interruptions in our operations, damage our reputation and deter clients and consumers from ordering our products and services. It could also result in litigation, the termination of client contracts, government inquiries and/or enforcement actions.

We have implemented a risk-based information/cybersecurity program dedicated to protecting our data and solutions. Our privacy policies, together with associated controls and procedures, provide a comprehensive framework to inform and guide the handling of data. These programs dovetail with our information security program in a manner designed to protect the data we handle. We employ an in-depth defensive strategy, utilizing the concept of security layers and the CIA (confidential, integrity and availability) triad model. Our information security program is led by our Chief Information Security Officer and the Information Security department, which establishes the policies, standards and strategies to manage security risk. We devote significant resources to addressing security vulnerabilities through enhancing security and reliability features in our products and services, reviewing and auditing our systems against independent security control frameworks, such as ISO 27001, and performing security maturity assessments, which inform our annual and multi-year cybersecurity strategies and our product security plans.

We have an Enterprise Risk Management Committee that is led by our Assurance and Risk Advisory Services group, our Chief Financial Officer and our Chief Administrative Officer, with participation from our executive leadership team and senior-level staff, including our Chief Compliance Officer and our Chief Information Security Officer. This committee assesses and monitors our top enterprise risks, including cybersecurity, and provides quarterly updates to our board of directors. Our Chief Information Security Officer also provides periodic updates to our board of directors, which is responsible for ensuring that we have implemented appropriate risk mitigation strategies, systems, processes and controls.

7

In the event a cybersecurity incident is identified, our Cybersecurity Incident Response team will act in accordance with our Incident and Crisis Management Program to communicate to our executive leadership team and to coordinate the response to any incident. Our Chief Executive Officer, Chief Financial Officer, General Counsel, Chief Information Security Officer and Chief Compliance Officer are responsible for assessing such incidents for materiality, ensuring that any required notification or communication occurs and determining, among other things, whether any prohibition on the trading of our common stock by insiders should be imposed prior to the disclosure of information about a material cybersecurity event. We maintain cybersecurity insurance coverage that insures us for costs resulting from cyberattacks, although this coverage may not reimburse us for all losses.

For more information on risks related to data security, see Item 1A, "Operational Risks – Security breaches, computer malware or other cyberattacks involving the confidential information of our customers, employees or business partners could substantially damage our reputation, subject us to litigation and enforcement actions, and substantially harm our business and results of operations."

| OUR MATERIALS, SUPPLIES AND SERVICE PROVIDERS | ||

The principal materials used in producing our main products are paper, plastics, ink, corrugated packaging and printing plate material, which we purchase from various sources. We also purchase stock business forms and promotional apparel produced by third parties. In addition, we have entered into agreements with third-party providers for delivery services and information technology services, including telecommunications, network server and transaction processing services, as well as various other services. We also rely on third parties to provide a portion of the data used to maintain our proprietary and non-proprietary databases, including credit and non-credit data from the national credit bureaus and other data brokers.

We have engaged a third-party global sourcing group to help manage our supply chain. We believe that in the event one of our vendors fails to perform, we would be able to obtain an alternative source of supply. However, with recent stresses on the global supply chain and labor market, we are taking steps to secure multiple sources of supply for certain of the materials and services we utilize, including those related to certain higher margin printed products in our Promotional Solutions segment. We can provide no assurance that we would be able to obtain an alternative source of supply, or that such supply could be obtained at current prices, in the event one of our vendors fails to perform.

| OUR HUMAN CAPITAL | ||

Our most valuable asset is our employee-owners. As of December 31, 2022, we had 5,863 employees, with 5,310 employees in the United States, 528 employees in Canada and the remainder located in Europe. Approximately 98% of our team is full-time employees, with 59% representing non-exempt roles working in production, processing or call center functions. We are proud of our strong history of positive, productive employee relations. None of our employees are currently represented by labor unions.

The foundation of our continuing success as a Trusted Payments and DataTM company is our ability to attract and retain diverse, exceptional and motivated talent. We accomplish this by providing a culture of inclusion, diversity, equity, development, opportunity and empowerment.

Results-Driven, Community-Focused, Collaborative Culture

We focus on creating an environment where our employee-owners, also known as Deluxers, feel respected and valued, and where they can contribute to their full potential. To this end, an important component of our strategy is that all North American employees are granted restricted stock unit awards. Our heritage also reflects deep-seated roots in community support and volunteerism, which is reflected in our purpose statement: “Champions for business so communities thrive.” Additionally, our values focus on delivering results:

•Customers First

•Earn Trust

•Innovation

•Grit and Perseverance

•Power of One

In an effort to continue to improve our culture and engagement, we provide learning and development at all levels of the organization on a variety of topics, including, leadership development, mentoring, and diversity, equity and inclusion. We continue to focus on training and development programs and transparent communication channels through change pulse checks, surveys, senior leadership forums and employee resource groups. We also provide a tool that allows for anonymous feedback directly from employees to management on new ideas, concerns and questions.

8

Diversity, Equity and Inclusion

We embrace DEI in our workforce, customers and partners, valuing their unique backgrounds, experiences, thoughts and talents. Our mission is to empower all employees to bring their full authentic selves to work and to foster an environment that reflects the diverse communities we serve. We strive to cultivate a culture and vision that supports and enhances our ability to recruit, develop and retain diverse talent at every level. We provide our customers, partners, and shareholders information about our DEI program and our activities supporting social justice within the communities we serve. In addition, we are focused on furthering our DEI initiatives throughout our business and have, among other things, created a DEI council that is sponsored by our Chief Human Resources Officer. This council is comprised of employee-owners across multiple functions and business segments. Its top priorities include implementing a comprehensive DEI learning and development plan to build awareness and drive inclusive behaviors; further developing our diversity pipeline through hiring, mentoring and coaching; and establishing goals and metrics to ensure progress.

As of December 31, 2022, our total workforce was approximately 56% female and 44% male. Our team members located in the United States were comprised of approximately 55% white, 16% Black or African American, 11% Hispanic or Latino, 10% Asian American and 8% other. We continue to focus our development and DEI programs on growing the number of female and minorities represented in leadership roles.

Under the board’s oversight and guidance, we have taken significant actions to enhance our diverse and inclusive culture, protect and train our employees, and maintain our reputation as a great place to work. We continually strive to improve the attraction, retention, and advancement of diverse employees to grow and retain talent that represents the communities in which we operate. Below are some recent examples of our commitment to DEI.

•33% of our directors identify as from diverse backgrounds, including the independent chair of our board, who is a woman of color.

•In 2020, we formed our employee resource committee and established 4 employee resource groups ("ERGs") dedicated to fostering inclusion and diversity. Since 2020, we have grown our programs and now offer 9 ERGs, including African American, Pacific Islander Middle Eastern Asian, disabled, Hispanic and Latino, veteran, LGBTQ+, parent and women.

•In 2022, we earned the honor of becoming a Yellow Ribbon Company, a designation awarded by the state of Minnesota to those companies meeting the top criteria for supporting veterans and their families.

•In 2022, we earned a top score of 100 on the Disability Equality Index and were named a “Best Place to Work for Disability Inclusion” for the third year in a row.

•In 2022, The Human Rights Campaign Foundation’s Corporate Equality Index recognized us as a Best Place to Work for the LGBTQ+ Equality.

Health, Wellness and Safety

Creating a culture where all employee-owners feel supported and valued is paramount to our strategy. We continue to monitor developments related to COVID-19 and its variants, and we continue to take steps to ensure the safety of our employees and business partners. We also continue to provide a competitive benefits package focused on fostering work/life integration. Well-being in our organization is about having a holistic commitment to provide resources and support for our employees so that they can deliver for customers and shareholders. We offer several programs to benefit our employees and support work environments that encourage growth, innovation, and productivity. These benefits range from standard medical, dental, life and disability insurance to programs that provide additional support for our employees' mental, physical, financial and social wellbeing. We provide paid parental leave and infertility, adoption and surrogacy assistance. We partner with Care.com® to offer services for employees to find tutors, nannies, children’s daycare and eldercare, and we offer an employee assistance program that provides employees with confidential counseling. We also offer employees tuition and travel assistance, and qualified long-term employees have the opportunity to take a sabbatical. Beginning in 2023, we began offering unlimited flexible time off to our salaried employees. By enabling our employees to thrive in their personal lives, we provide tools for our employees to best deliver for customers and shareholders while at work.

Community Engagement

Our employee-owners believe in the power of connection, of activity and of giving back to the communities we serve. Our partnerships and charitable work in the communities we serve are an integral part of our core values. This spirit of community is felt throughout our organization and is fostered by our paid volunteer time off (VTO) program for employees, which provides three paid VTO days per year. It is also reflected in our partnership with the Deluxe Foundation, which enables employees to donate to not-for-profit organizations of their choosing and receive a matching donation, dollar for dollar, up to $2,000 per year. Our commitments go beyond monetary donations. Several of our top executives serve on boards for major not-for-profit organizations and other community organizations that align with our company values of diversity initiatives, rebuilding communities and education.

9

We continue our commitment to enriching our communities in the following ways:

•Since 1992, we have partnered with Junior Achievement USA® chapters in our local communities to inspire and prepare young people to succeed. We support Junior Achievement’s mission through foundation grants, awareness and employee volunteers.

•We have partnered with the American Red Cross® for decades, organizing blood drives at our locations and hosting fundraisers and bake sales to help fund the American Red Cross mission of preventing and alleviating human suffering in the face of emergencies.

•In 2022, in partnership with Habitat for Humanity®, we helped build new homes across the country, including inviting our technology partners to join us on a two day build in Chaska, Minnesota.

•For Black History Month in 2022, we partnered with the Minnesota Timberwolves and Minnesota Lynx to film an original YouTubeTM series called “The Come Up,” that focused on highlighting the significance of black excellence and the importance of uplifting the black community.

•Our employees pledged $133,000 in donations under our 2022 employee giving campaign.

•In 2022, our employees contributed more than 22,500 hours to our local communities through our VTO program.

| SEASONALITY | ||

Historically, we have experienced seasonal trends with some of our products and services. For example, Promotional Solutions holiday card and revenues from certain marketing services in Data Solutions are typically stronger in the fourth quarter of the year due to the holiday season, while sales of Promotional Solutions tax forms are stronger in the first and fourth quarters of the year. Our customers' marketing campaign cycles may also result in some revenue fluctuations for these segments.

| GOVERNMENT REGULATION | ||

We are subject to numerous international, federal, state and local laws and regulations that affect our business activities in several areas, including, but not limited to, labor, advertising, taxation, data privacy and security, digital content, consumer reports, consumer protection, merchant processing, online payment services, real estate, e-commerce, intellectual property, health care, environmental matters, and workplace health and safety. The complexity of complying with existing and new laws and regulations is significant, and regulators may adopt new laws or regulations at any time.

For more specific information about the effects of government regulation on our business, see Item 1A, "Legal and Compliance Risks – Governmental regulation is continuously evolving and could limit or harm our business." We believe that the impact on our capital expenditures and earnings of complying with government regulations will not be materially different in the upcoming year than it was in 2022.

| AVAILABLE INFORMATION | ||

We make available, without charge, through our investor relations website, www.investors.deluxe.com, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or furnished pursuant to section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after these items are electronically filed with or furnished to the SEC. These reports can also be accessed via the SEC website, www.sec.gov.

A printed copy of this report may be obtained without charge by calling 651-787-1068, by sending a written request to the attention of Investor Relations, Deluxe Corporation, P.O. Box 818095, Cleveland, Ohio 44181, or by sending an email request to investor.relations@deluxe.com.

Further information about Deluxe Corporation is also available at www.deluxe.com, www.facebook.com/deluxecorp, www.linkedin.com/company/deluxe and www.twitter.com/deluxe. The content of these websites is not incorporated by reference in this Annual Report on Form 10-K or in any other report or document we file with the Securities and Exchange Commission.

| OUR CODE OF ETHICS AND CORPORATE GOVERNANCE GUIDELINES | ||

We have adopted a Code of Ethics that applies to all of our employees and our board of directors. The Code of Ethics is available on our investor relations website, www.investors.deluxe.com, and also can be obtained free of charge upon written request to the attention of Investor Relations, Deluxe Corporation, P.O. Box 818095, Cleveland, Ohio 44181. Any changes or

10

waivers of the Code of Ethics will be disclosed on our website. In addition, our Corporate Governance Guidelines and the charters of the Audit, Compensation, Corporate Governance and Finance Committees of our board of directors are available on our website, www.investors.deluxe.com, or upon written request.

| INFORMATION ABOUT OUR EXECUTIVE OFFICERS | ||

Our executive officers are appointed by the board of directors each year. The following summarizes our executive officers and their positions.

| Name | Age | Present Position | Executive Officer Since | ||||||||

| Barry McCarthy | 59 | President and Chief Executive Officer | 2018 | ||||||||

| William "Chip" Zint | 37 | Senior Vice President, Chief Financial Officer | 2022 | ||||||||

| Garry Capers, Jr. | 46 | Senior Vice President, Division President, Data Solutions and Promotional Solutions | 2019 | ||||||||

| Jeffrey Cotter | 55 | Senior Vice President, Chief Administrative Officer and General Counsel |

2018 | ||||||||

| Tracey Engelhardt | 58 | Senior Vice President, Division President, Checks and Chief of Operations | 2012 | ||||||||

| Jean Herrick | 54 | Senior Vice President, Chief Human Resources Officer | 2022 | ||||||||

| Yogaraj "Yogs" Jayaprakasam | 45 | Senior Vice President, Chief Technology and Digital Officer | 2022 | ||||||||

| Amanda Parrilli | 44 | Senior Vice President, Chief Strategy, Transformation and Business Development Officer | 2019 | ||||||||

| Michael Reed | 51 | Senior Vice President, Division President, Payments | 2019 | ||||||||

Barry McCarthy joined us in November 2018 as President and Chief Executive Officer. Prior to joining us, Mr. McCarthy served in various senior executive positions, most recently, from November 2014 to November 2018, as Executive Vice President and Head of Network and Security Solutions, a segment of publicly traded First Data Corporation, a financial services company, now part of Fiserv, Inc.

Chip Zint joined us in August 2020 as Vice President of Corporate Finance and was named Senior Vice President, Chief Financial Officer in October 2022. Prior to joining us, Mr. Zint held several positions with NCR Corporation, an enterprise technology provider, most recently as Vice President of Finance and Chief Financial Officer of Hardware from January 2019 to July 2020 and Vice President, Corporate Financial Planning and Analysis from May 2017 to January 2019.

Garry Capers, Jr. joined us in September 2019 as Senior Vice President, Division President, Data Solutions, and in November 2021, added the Promotional Solutions segment to his responsibilities. Prior to joining us, Mr. Capers was employed by Automatic Data Processing, Inc., a provider of human resources management software and services, from January 2017 to September 2019, most recently as Senior Vice President, General Manager, National Account Services Comprehensive Outsourcing Services and Operations.

Jeffrey Cotter was named Chief Administrative Officer in January 2019. Mr. Cotter joined us in June 2018 as Senior Vice President, General Counsel. Prior to joining us, Mr. Cotter served as Senior Vice President and General Counsel for Tennant Company, a provider of cleaning products and solutions, from September 2017 to June 2018.

Tracey Engelhardt was named Senior Vice President, Division President, Checks in October 2019 and in May 2022, she added Chief of Operations to her responsibilities. From March 2017 to October 2019, Ms. Engelhardt served as Senior Vice President, Direct-to-Consumer.

Jean Herrick was named Senior Vice President, Chief Human Resources Officer in June 2022. From January 2016 to June 2022, Ms. Herrick served as Vice President, Human Resources.

Yogs Jayaprakasam joined us in May 2022 as Senior Vice President, Chief Technology and Digital Officer. Prior to joining us, Mr. Jayaprakasam held several positions with American Express Company, most recently as Unit Chief Information Officer for the Global and Large Client Group and head of engineering for B2B Digital Payments from June 2021 to May 2022. Mr. Jayaprakasam also served American Express Company as Vice President, Enterprise Platforms for Sales, Marketing and Data Platforms from May 2020 to June 2021, and as Vice President, Enterprise Platforms for Sales and Marketing from November 2017 to May 2020.

Amanda Parrilli was named Senior Vice President, Business Development and Strategy in October 2019, and in June 2020, she added Transformation to her responsibilities. Ms. Parrilli joined us in February 2019 as Vice President, Strategy. Prior

11

to joining us, Ms. Parrilli held several positions at The Home Depot, Inc., most recently as Senior Director, Services Lead Generation from January 2018 to February 2019.

Michael Reed joined us in November 2019 as Senior Vice President, Division President, Payments. Prior to joining us, Mr. Reed served as Managing Director, Global Payments and Product for Barclays Bank Plc in London from September 2018 to November 2019. From January 2015 to August 2018, Mr. Reed served as Managing Director at BofA Merrill Lynch Merchant Services (Europe) Limited, the European subsidiary of Banc of America Merchant Services, LLC.

| ITEM 1A. RISK FACTORS | ||||||||||||||

We routinely encounter and address risks, many of which could cause our future results to be materially different than we currently anticipate. These risks include, but are not limited to, the principal factors listed below and the other matters set forth in this Annual Report on Form 10-K. We place no priority or likelihood based on these descriptions or order of presentation. We are also subject to general risks and uncertainties that affect many other companies, including overall economic, industry and market conditions. Additional risks not presently known to us, or that we currently believe are immaterial, may also adversely affect us. You should carefully consider all of these risks and uncertainties before investing in our common stock.

| STRATEGIC RISKS | ||

If our long-term growth strategy is not successful, our business and financial results would be adversely impacted.

Our vision is to be a trusted technology partner empowering businesses to pay, get paid and grow. Further information about our strategy can be found under the caption "Our Strategy" appearing in Part I, Item 1 of this report. We may not achieve our long-term objectives, and investments in our business may fail to impact our financial results as anticipated. Our strategic plan could fall short of our expectations for many reasons, including, among others:

•our failure to generate profitable revenue growth;

•our inability to acquire new customers, retain our current customers and sell more products and services to current and new customers;

•our failure to fully utilize new sales technology that enables a single view of our customers;

•our inability to implement additional improvements to our technology infrastructure, our digital services offerings and other key assets to increase efficiency, enhance our competitive advantage and scale our operations;

•our failure to develop new products and services;

•our failure to effectively manage the growth, expanding complexity and pace of change of our business and operations;

•our inability to effectively operate, integrate or leverage businesses we acquire;

•the failure of new products and services to achieve widespread customer acceptance;

•our inability to promote, strengthen and protect our brand;

•an unexpected change in demand for checks or other products;

•our failure to attract and retain skilled talent to execute our strategy and sustain our growth;

•unanticipated changes in our business, markets, industry or the competitive landscape; and

•general economic conditions.

We can provide no assurance that our strategy will be successful, either in the short term or in the long term, that it will generate a positive return on our investment or that it will not materially reduce our adjusted earnings before interest, taxes, depreciation and amortization (adjusted EBITDA) margins. If our strategy is not successful, or if there is market perception that our strategy is not successful, our reputation and brand may be damaged and our stock price may fall.

If we are unable to attract and retain customers in a cost-effective manner or effectively operate a multichannel customer experience, our business and results of operations would be adversely affected.

Our success depends on our ability to attract new and returning customers in a cost-effective manner. We use a variety of methods to promote our products and services, including a direct sales force, partner referrals, email marketing, purchased search results from online search engines, direct mail advertising, broadcast media, advertising banners, social media and other online links. Certain of these methods may become less effective or more expensive. For example, response rates for direct mail advertising have been decreasing for some time, internet search engines could modify their algorithms or increase prices for purchased search results or certain partner referrals could decline. Because we offer a diverse portfolio of products and services, we may also face challenges in increasing customer awareness of all of our offerings. Efforts to expand customer awareness of our diverse range of products and services may result in increased marketing expense and may fail to generate additional revenue.

We continually evaluate and modify our marketing and sales efforts to achieve the most effective mix of promotional methods. Competitive pressure may inhibit our ability to reflect increased costs in the prices of our products and services and/or

12

new marketing strategies may not be successful. Either of these occurrences would have an adverse impact on our ability to compete and our results of operations would be adversely affected. In addition, when our check supply contracts expire, customers have the ability to renegotiate their contracts with us or to consider changing suppliers. Failure to achieve favorable contract renewals and/or to obtain new check supply customers would result in decreased revenue.

Additionally, we believe we must maintain a relevant, multichannel experience in order to attract and retain customers. Customers expect to have the ability to choose their method of ordering, whether via the mail, computer, phone or mobile device. Although we are constantly investing in our user experience, we cannot predict the success of these investments. Multichannel marketing is rapidly evolving and we must keep pace with the changing expectations of our customers and new developments by our competitors. If we are unable to implement improvements to our customer-facing technology in a timely manner, or if our customer-facing technology does not function as designed, we could find it increasingly difficult to attract new and returning visitors, which would result in decreased revenue.

We face intense competition from other business enterprises, and we expect that competition will continue to increase.

Competition in the payments industry is intense. We are competing against numerous financial technology (Fintech) companies, including independent payment processors, credit card processing firms and treasury management service providers, as well as financial institution in-house capabilities. Volume is the key to staying cost-competitive, and breadth of services is critical to staying relevant to customers. In addition, although we are a leading check printer in the U.S., we face considerable competition in the check printing portion of the payments industry from another large check printer in our traditional financial institution sales channel, from direct mail and internet-based sellers of personal and business checks, from check printing software vendors, and from certain significant retailers. Pricing continues to be competitive in our financial institution sales channel, as financial institutions seek to maintain their previous levels of profitability, even as check usage declines.

Within our Data Solutions segment, our data-driven marketing services face intense competition from a wide variety of companies in the data solutions space, including advertising agencies, marketing technology firms, data aggregators and brokers, and source data providers. Adapting to new technology is a key challenge in this business, along with hiring and retaining the right people.

Within our Promotional Solutions segment, the markets for business forms and promotional products are intensely competitive and highly fragmented. Current and potential competitors include traditional storefront printing companies, office superstores, wholesale printers, online printing companies, small business product resellers and providers of custom apparel and gifts. The competitive landscape for online suppliers continues to be challenging as new businesses enter the space.

We can provide no assurance that we will be able to compete effectively against current and future competitors. Our competitors may develop better products or technologies and may be able to adapt more quickly to new or emerging technologies and changes in customer requirements. Continued competition could result in price reductions, reduced profit margins and/or loss of customers, all of which would have an adverse effect on our results of operations and cash flows.

If we do not adapt to changes in technology in a timely and cost-effective manner, we could lose clients or have trouble attracting new clients, and our ability to grow may be limited.

Rapid, significant, and disruptive technological changes impact the markets for our products and services, including changes in payment and internet browser technologies and the use of artificial intelligence and machine learning, as well as developments in technologies supporting our regulatory and compliance obligations and in-store, digital, mobile and social commerce. The introduction of competing products and services using new technologies, the evolution of industry standards or the introduction of more attractive products or services, including continued increases in the digitization of payments, could make some of our products and services less desirable, or even obsolete. Our ability to enhance our current products and services and to develop and introduce innovative products and services will significantly affect our future success. The impact is magnified by the intense competition we face. To be successful, our technology-based products and services must keep pace with technological developments and evolving industry standards, address the ever-changing and increasingly sophisticated needs of our customers, and achieve market acceptance. Additionally, we must differentiate our service offerings from those of our competitors and from the in-house capabilities of our customers. We could lose current and potential customers if we are unable to develop products and services that meet changing demands in a timely manner. Additionally, we must continue to develop our skills, tools and capabilities to capitalize on existing and emerging technologies, and this requires significant investment, takes considerable time and ultimately, may not be successful. Any of the foregoing risks could result in harm to our business, results of operations and growth prospects.

We may be unable to successfully identify future acquisitions, integrate past and future acquisitions and realize the anticipated benefits of the transactions.

We have completed many acquisitions during the past several years, including the acquisition of First American in June 2021, which was the largest acquisition in our history. In addition, we purchased the operations of several small business distributors with the intention of growing revenue in our dealer channels. We are currently devoting significant management

13

attention and resources to integrating the business practices and operations of First American and our previous acquisitions. The integration of any acquisition involves numerous risks, including, among others:

•the inability to successfully combine the businesses in a manner that permits us to achieve the revenue synergies and cost savings anticipated to result from the acquisition, which would result in the anticipated benefits of the acquisition not being realized in the anticipated timeframe or at all;

•difficulties and/or delays in assimilating operations and ensuring that a strong system of information security and controls is in place;

•the complexities of integrating a company with different products, services, markets and customers;

•performance shortfalls due to the diversion of management's attention from other business concerns;

•lost sales and customers as a result of certain customers, retail partners, financial institutions or other third parties deciding not to do business with us;

•unanticipated integration costs;

•complexities associated with implementing necessary controls for the acquired business activities to address our requirements as a public company;

•difficulties in identifying and eliminating redundant and underperforming functions and assets;

•the complexities of assimilating the acquired business into our corporate culture and management philosophies;

•unidentified issues not discovered during our due diligence process, including product or service quality issues, intellectual property issues and tax or legal contingencies;

•failure to address legacy distributor account protection rights; and

•loss of key employees.

One or more of these factors could impact our ability to successfully operate, integrate or leverage an acquisition and could materially and adversely affect our business and financial results.

We have indicated that we plan to supplement sales-driven revenue growth with strategically targeted acquisitions over time. The time and expense associated with finding suitable businesses, technologies or services to acquire can be disruptive to our ongoing business and may divert management’s attention. We cannot predict whether suitable acquisition candidates can be identified or acquired on acceptable terms or whether any acquired products, technologies or businesses will contribute to our revenue or earnings to any material extent. We may need to seek additional financing for larger acquisitions, which would increase our debt obligations and may not be available on terms that are favorable to us. Additionally, acquisitions may result in additional contingent liabilities, additional amortization expense, and/or future non-cash asset impairment charges related to acquired intangible assets and goodwill, and thus, could adversely affect our business, results of operations and financial condition.

The use of checks and forms is declining and we may be unable to offset the decline with profitable revenue growth.

Checks continue to be a significant portion of our business, accounting for 32.6% of our consolidated revenue in 2022, and providing a significant amount of the cash flows we invest in our growth businesses, although our Payments segment now rivals our Checks segment in terms of revenue. We sell checks for personal and business use and believe that there will continue to be demand for personal and business checks for the foreseeable future, although the total number of checks written in the U.S. has been in decline since the mid-1990s. We expect that the number of checks written will continue to decline due to the digitization of payments, including debit cards, credit cards, direct deposit, wire transfers, and other payment solutions, such as PayPal®, Apple Pay®, Square®, Zelle®, and Venmo®, as well as cryptocurrencies. In addition, the RTP® system run by The Clearing House Payments Company, LLC is a real-time payments system that currently reaches approximately 60% of U.S. bank accounts. The U.S. Federal Reserve has announced that it plans to develop its own real-time payments system, FedNowSM, with an expected launch in mid-2023.

The rate and the extent to which digital payments will replace checks, whether as a result of legislative developments, changing payment systems, personal preference or otherwise, cannot be predicted with certainty. Increased use of alternative payment methods, or our inability to successfully offset the secular decline in check usage with new check supply clients or other sources of revenue, would have an adverse effect on our business, cash flows and results of operations.

The use of business forms has also been declining. Continual technological improvements, including the lower price and higher performance capabilities of personal computers, printers and mobile devices, have provided small business customers with alternative means to execute and record business transactions. Additionally, electronic transaction systems, off-the-shelf business software applications, web-based solutions and mobile applications have been designed to replace preprinted business forms. Greater acceptance of electronic signatures also has contributed to the overall secular decline in printed products. It is difficult to predict the pace at which these alternative products and services will replace standardized business forms. If small business preferences change rapidly and we are unable to develop new products and services with comparable operating margins, our results of operations would be adversely affected.

14

Our business depends on our strong and trusted brand, and any failure to maintain, protect and enhance our brand would hurt our business.

We have developed a strong and trusted brand that has contributed significantly to the success of our business. We believe that maintaining and promoting our brand in a cost-effective manner is critical to achieving widespread acceptance of our products and services, expanding our base of customers, and attracting and retaining top talent throughout the organization. We believe that the importance of brand recognition and trust is particularly essential for the success of our various service offerings because of the level of competition for these services. Customer awareness of our brand, as well as the perceived value of our brand, depends largely on the success of our marketing efforts, our ability to continue to provide useful, reliable, secure and innovative products and services, and our ability to maintain trust and be a technology leader. If we fail to successfully promote and maintain our brand or if we incur excessive expenses in this effort, our business could be materially and adversely affected. There is also the risk that adverse publicity, whether or not justified, could adversely affect our business. If our business partners or key employees are the subject of adverse news reports or negative publicity, our reputation may be tarnished and our results of operations could be adversely affected.

A component of our brand promotion strategy is building on our relationship of trust with our customers, which we believe can be achieved by providing a high-quality customer experience. We have invested, and will continue to invest, in website development, design and technology, and customer service and production operations. Our ability to provide a high-quality customer experience is also dependent on external factors, including the reliability and performance of our suppliers, telecommunications providers and third-party carriers. Our brand value also depends on our ability to protect and use our customers' data in a manner that meets expectations. The failure of our brand promotion activities to meet our expectations or our failure to provide a high-quality customer experience for any reason could adversely affect our ability to attract new customers and maintain customer relationships, which would adversely harm our business and results of operations.

Our cost reduction initiatives may not be successful.

Intense competition and secular declines in the use of checks and business forms compels us to continually improve our operating efficiency in order to maintain or improve profitability. Cost reduction initiatives have required, and will continue to require, up-front expenditures related to various actions, such as redesigning and streamlining processes, consolidating information technology platforms, standardizing technology applications, further enhancing our strategic supplier sourcing arrangements, improving real estate utilization and funding employee severance benefits. We can provide no assurance that we will achieve future cost reductions or that we will do so without incurring unexpected or greater than anticipated expenditures. Moreover, we may find that we are unable to achieve business simplification and/or cost reduction goals without disrupting our business, negatively impacting efforts to grow our business or reducing the effectiveness of our sustainability practices. As a result, we may choose to delay or forgo certain cost reductions as business conditions require. Failure to continue to improve our operating efficiency and to generate adequate savings to fund necessary investments could adversely affect our business if we are unable to remain competitive.

| OPERATIONAL RISKS | ||

We are unable to predict the extent to which COVID-19 or other outbreaks, epidemics, pandemics, or public health crises may adversely impact our business, financial condition and results of operations.

Although the immediate impacts of the COVID-19 pandemic have declined, the sweeping nature of the pandemic makes it extremely difficult to predict how our business and operations may be affected in the longer term. The extent to which COVID-19 continues to impact our business depends on future developments, many of which are unknown, such as: the severity and duration of the pandemic, including the impact of COVID-19 variants; governmental, business and individuals' actions in response to the pandemic; vaccination rates; and the resulting impact on economic activity and the financial markets. There are no comparable recent events that provide guidance as to the effect the COVID-19 pandemic may have, and, as a result, the ultimate impact of the pandemic is highly uncertain and subject to change.

In addition to the above impacts, at the onset of the COVID-19 pandemic in 2020, all of our employees who had the ability to work from home did so, and the success of our work-from-home model allowed us to accelerate certain site closures. Although our facilities re-opened in late 2021, a portion of our employees now work remotely on a permanent basis and many others work remotely for portions of each work week, which increases our cybersecurity and data security risk. Changes in the scope and severity of the pandemic may cause us to once again close certain of our facilities to protect the health of our employees, as a result of disruptions in the operation of our supply chain, or in response to a prolonged decrease in demand for our products and services. Disruptions caused by future facility closures, along with the subsequent reintroduction of employees back into the workplace, could introduce operational risks, negatively impact productivity or result in claims by employees.

Other cascading effects of the COVID-19 pandemic, along with other outbreaks, epidemics, pandemics or public health crises that are not currently foreseeable, could materially increase our costs, negatively impact our revenue and adversely impact our results of operations and liquidity, possibly to a significant degree. We cannot predict the severity or duration of any

15

such impacts. Such events could have the effect of heightening or exacerbating many of the other risks described in this Risk Factors discussion.

Security breaches, computer malware or other cyberattacks involving the confidential information of our customers, employees or business partners could substantially damage our reputation, subject us to litigation and enforcement actions, and substantially harm our business and results of operations.

Information security risks have increased in recent years, in part because of the proliferation of new technologies and an increase in remote work arrangements, as well as the increased sophistication and activities of hackers, terrorists and activists. In addition, our information security risks have increased with the acquisition of companies with their own technologies, which we continue to integrate into our systems and processes. Until these technologies are integrated, we may experience a period of increased risk. We use internet-based channels that collect customers’ financial account and payment information, as well as other sensitive information, including proprietary business information and personally identifiable information of our customers, employees, contractors, suppliers and business partners. Each year, we process hundreds of millions of records containing data related to individuals and businesses. We also provide services that are instrumental in supporting our customers and their businesses, such as website/email hosting and remittance processing. Cybersecurity is one of the top risks identified by our Enterprise Risk Management Committee, as technology-based organizations such as ours are vulnerable to targeted attacks aimed at exploiting network and system weaknesses.

The secure and uninterrupted operation of our networks and systems, as well as the processing, maintenance and confidentiality of the sensitive information that resides on our systems, is critical to our business operations and strategy. We have a risk-based information/cybersecurity program dedicated to protecting our data and solutions. We employ a defensive in-depth strategy, utilizing the concept of security layers and the CIA (confidential, integrity and availability) triad model. Computer systems and networks are, by nature, vulnerable to unauthorized access. An accidental or willful security breach could result in unauthorized access and/or use of customer information, including consumers' personally identifiable information or, in some cases, the protected health information of certain individuals. Our security measures could be breached by third-party action, computer viruses, accidents, employee or contractor error, or malfeasance by rogue employees. In addition, we depend on a number of third parties, including vendors, developers and partners, that are critical to our business and to which we may grant access to our customer or employee data. While we conduct due diligence on these third parties with respect to their security and business controls, we rely on them to effectively monitor and oversee these control measures. Individuals or third parties may be able to circumvent controls and/or exploit vulnerabilities that may exist, resulting in the disclosure or misuse of sensitive business and personal customer or employee information and data.

We utilize third-party providers to help support and provide our services to customers. We have established a vendor security program that assesses the risk of these partners, and certain of our third-party relationships are subject to security requirements as specified in written contracts. However, we cannot control the actions of our third-party providers, and any cyberattacks or security breaches they experience could adversely affect our ability to service our customers or otherwise conduct our business.

Because techniques used to obtain unauthorized access, disable or degrade service, or sabotage computer systems change frequently, may be difficult to detect immediately, and generally are not recognized until they are launched against a target, we may be unable to implement adequate preventive measures. Unauthorized parties may also attempt to gain access to our systems or facilities through various means, including hacking into our systems or facilities, fraud, trickery or other means of deceiving employees and contractors. We have experienced external internet-based attacks by threat actors aimed at disrupting internet traffic and/or attempting to place illegal or abusive content on our or our customers’ websites. Additionally, our customers and employees have been and will continue to be targeted by threat actors using social engineering techniques to obtain confidential information or using fraudulent "phishing" emails to introduce malware into the environment. To-date, these various threats and incidents have not materially impacted our customers, our business or our financial results. However, our technologies, systems and networks are likely to be the target of future attacks due to the increasing threat landscape for all technology businesses, and we can provide no assurance that future incidents will not be material.

Despite our significant cybersecurity systems and processes, a party that circumvents our security measures could misappropriate our own, our customers' or our partners' personal or proprietary information, cause interruption in our operations, damage our computers or those of our users, or otherwise damage our reputation, all of which could deter clients and consumers from ordering our products and services and result in the termination of client contracts. Additionally, it is possible that there could be vulnerabilities that impact large segments of mobile, computer or server architecture. Any of these events would adversely affect our business, financial condition and results of operations.

In addition, if we were to experience a material information security breach, we may be required to expend significant amounts of management time and financial resources to remedy, protect against or mitigate the effects of the breach, and we may not be able to remedy the situation in a timely manner, or at all. Furthermore, under payment card association rules and our contracts with debit and credit card processors, if there is a breach of payment card information that we store or that is stored by third parties with which we do business, we could be liable to the payment card issuing banks for their cost of issuing new cards and other related expenses. We could also lose our ability to accept and process credit and debit card payments, which would likely result in the loss of customers and the inability to attract new customers. We could also be exposed to time-consuming and

16

expensive litigation, government inquiries and/or enforcement actions. If we are unsuccessful in defending a claim regarding information security breaches, we may be forced to pay damages, penalties and fines, and our insurance coverage may not be adequate to compensate us fully for any losses that may occur. Contractual provisions with third parties, including cloud service providers, may limit our ability to recover losses resulting from the security breach of a business partner.